IPCC Climate Change Mitigation Report

On April 4th, the IPCC released its third and final report on climate change mitigation measures. In this article, we present key insights from the energy sector, which has seen its emissions increase since the Paris Agreement despite efforts that should result in lower carbon intensity for energy systems. Nuclear energy is thoroughly, yet discretely documented in the IPCC report. There are two reasons for this: On one hand, the report focuses on short-term measures (2030 objectives) which are incompatible with the pace of deployment for new nuclear plants. On the other hand, the report tends to express a global view, which does not allow for inferences to be made at a national level. In France for example, extending the operating life of its reactors remains the best option available from an emissions and economic perspective. Nonetheless, nuclear energy is considered the fourth most potential contributor to the decarbonization of energy systems.

The last edition of the Intergovernmental Panel on Climate Change (IPCC) report trilogy was released on April 4th with a publication dedicated to climate change mitigation measures. These reports are the result of three years of work by 278 scientists from 65 countries reviewing more than 18,000 publications. While the first two reports (The Physical Science Basis, and Impacts, Adaptation and Vulnerability respectively) reminded the world that climate change already exists, and that it is significantly impacting the biosphere and human society, this third report offers little more optimism.

According to the authors, our efforts – though significant[1] in many sectors and in many countries – are largely insufficient if the world is to limit global warming to 1.5°C. The figures are clear: to return to a 1.5°C trajectory by 2030, overall emissions must be reduced by 43%, and methane emissions by 34%. The less ambitious goal of a 2°C trajectory will see a peak in emissions in 2025 and a quarter reduction in emissions by 2030. At present, the planet is on a 3.2°C trajectory by the end of the century. Before detailing the solutions available on the supply side to change this trajectory, the report highlights the need to reduce the demand for carbon-intensive services, and thus decrease emissions. The message is clear: without quelling this demand, we will not succeed.

In the following section, we present key insights for the energy sector. In 2019, before the pandemic forced a reduction in emissions, this sector accounted for 34% of human-induced (anthropogenic) GHG emissions. Despite improvements in the sector’s carbon intensity, emissions – driven by rising demand – continue to rise.

Overview of energy sector emissions

The increase in GHG emissions since 2010 (although lower than the previous decade1) concerns all sectors, and the energy sector is no exception. The reduction in emissions linked to a decrease in the carbon intensity of energy[3] has not offset the overall increase in the sector’s activity. This reduction, estimated at around -0.3%/year over the 2010-2019 period, is primarily due to a shift from massive amounts of coal-fired power plants to gas-fired power plants, a reduction in coal growth and an increase in the uptake of renewable energy across energy systems. However, we are more than ten times below (-3.5%/year) the rate of energy system decarbonization that is needed to limit global warming to 2°C.

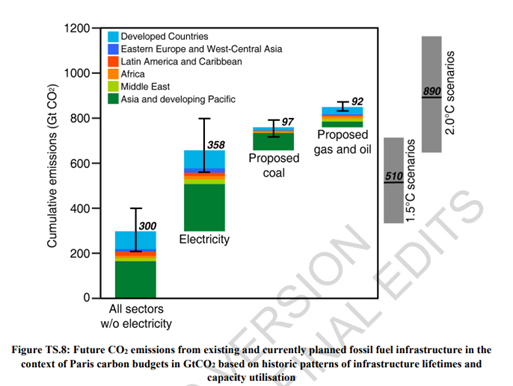

Increase in fossil fuels since the Paris Agreement

Since the 2015 Paris Agreement, emissions from the energy sector have increased by around 4.6%. Fossil fuels (oil, gas, and coal) are behind much of this increase: methane emissions – mainly due to leakage from the exploitation and transport of fossil products – account for 18% of these emissions. Coal power capacity grew by 7.6% – where consumption is expected to fall by 70% by 2030 – and gas consumption increased by 15%.

The report stresses that investment in fossil fuel assets[4] must end for two reasons. First, given the inaction of our energy systems, investment would remove the possibility of limiting global warming to 2°C. Second, investing in new assets (the crude resource or assets such as power plants), would have devastating macroeconomic impacts. For example, the cost of fuel and carbon per tonne can affect the profitability of a gas-fired power plant and thus put investors at financial risk or have a lasting impact on corporate and household energy supply (p.53 TS).

Limiting investment is of course not enough. We must reduce our dependence on fossil fuels by redirecting financial flows towards investment in the energy transition and towards low or zero-carbon systems, particularly if we want to respect the Paris Agreement framework. The report asserts that investment must be reduced by three to six times across all sectors. Based on a historical study of the exploitation of existing fossil fuel assets, the IPCC estimates that we have already exceeded the carbon budget to limit warming to 1.5°C.

Increased electrification is needed to assure the energy transition

Electrification is a critical instrument in the energy transition. The report stresses that by 2050, electricity will have to account for around 50% of total energy supply to limit warming to 1.5°C (it represented 20% in 2019). On average, the electricity systems of tomorrow will be mainly composed of Variable Renewable Energy Sources, wind and solar. The continuous decline in unit costs of these energy sources since 2010[5] has made these low-carbon technologies competitive against fossil fuels (gas, coal, etc.). In addition, public support for renewables creates a particularly favourable context for new investment opportunities in these energies.

Electrification requires increased renewable and nuclear energy

While (electric) energy systems share common characteristics, including those attributed to renewables due to their increasing potential for decarbonization,”it is unlikely that all low-carbon energy systems around the world will rely entirely on renewable energy sources,” outlines the report (p. 1071). The context of each country (box 6.6.4.) will be decisive when choosing complementary technologies.

Thus, while some countries want to be nuclear-free, others consider nuclear energy as a strategic asset (p. 640) for the transition in the medium and long term. As such, the report lists several nuclear options available over the 2020-2050 period: new reactor concepts, extending the life of existing nuclear power plants, and Small Modular Reactors (SMRs). In addition to electricity generation, nuclear energy can also contribute to sanitary water production or carbon-free hydrogen and has the potential to decarbonize certain industrial processes.

The necessary technology exists, and countries must decide which option is best in accordance with its needs

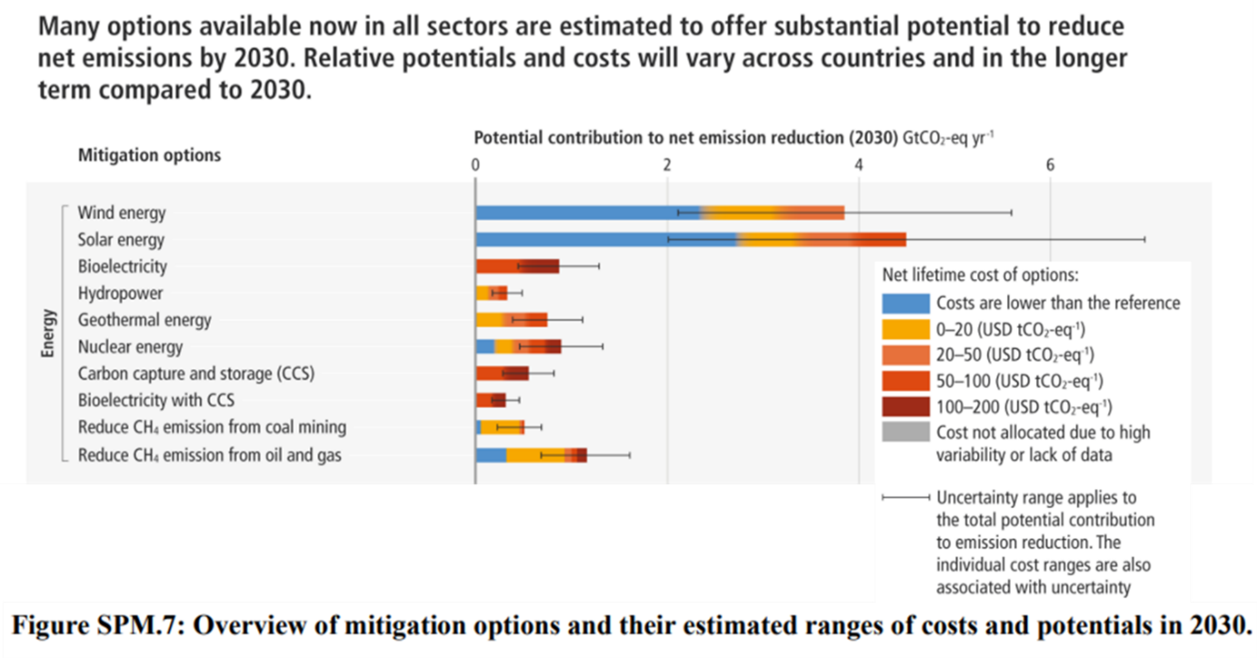

The policymakers’ summary shown in figure SPM.7 provides a comprehensive sector-by-sector list of mitigation options to reduce the net balance of our emissions by 2030 and their respective contributions. The options listed are already available, and therefore exclude new nuclear power plants whose positive effects on the climate (given their stagnant deployment) will only be appreciated from 2040. In France for example, the first EPR2s will only come into service from 2035.

For the energy sector, it is generally solar and wind that offer the greatest potential to reduce GHG emissions, to the tune of 4 GtCO2eq/year, by 2030. This is four to eight times the potential of nuclear power, which itself is two to three times more efficient than hydropower. But again, this is all “generally” speaking. While the report provides a broad view of the best options available, not all the insights gleaned from such a graph are directly applicable. For example, should we conclude from such a graph that Iceland, whose electricity comes from 100% hydropower and geothermal energy – decarbonized sources – has bad energy policy and must immediately invest in wide-scale wind power? Of course not.

To understand the interest in such a graph, we must place ourselves in the position of a country whose electricity sector is either low-carbon or poorly developed. According to previous IPCC reports, this country needs to urgently (1) electrify its systems and (simultaneously) (2) decarbonize its electricity mix. The figure above presents the most effective solutions to this challenge in the medium term (2030). So indeed, given the unit costs, market growth, and the ease of installation and maintenance, IRES should be favored in the short term.

However, for countries with nuclear power plants already in operation, it is necessary to continue investment in IRES, as well as consider extending the life of nuclear plants, for this is undoubtedly the cleanest (for climate and soil, or potential carbon sinks) and most economical solution today (IEA/NEA, 2020). Continuing investment in these two options is consistent with climate objectives since all available solutions must be considered.

Finally, the contribution of nuclear power to the Paris Agreement objectives only reaches its full potential in the long term (Table TS.2). 2030 is a short horizon for decisions such as investing in new nuclear reactors, which occurs over extended periods of time. The report estimates that in 2050, a doubling of nuclear capacity, or even a quadrupling of it (to stay below 1.5°C), serves as one of the possible routes necessary to reduce emissions.

This report should not be interpreted as saying what it does not

Comparing the cost per tonne avoided (Figure SPM.7) as an indicator, with that of the LCOE (Levelized Cost of Energy) has intrinsic methodological limitations. The IPCC report states in a footnote and under Figure SPM.3 that the costs per tonne of carbon avoided for solar and wind do not include system costs (flexibility, grid reinforcement, etc.). Therefore, this analysis should be onboarded with a certain level of scrutiny.

Despite being full of rich insights, the third IPCC report is not a forward-looking scenario analysis for electrical (or energy) systems. To draw insights on this topic, within the specific scope of France, we must look at the lessons of the RTE (French Electricity Transmission Network) report which uses the system costs methodology. Nuclear/intermittent complementary energy appears to be the most robust solution for decarbonization, and the most competitive solution for controlling energy costs for consumers.

Insights from the IPCC Report on Nuclear Energy and Future Prospects

The following conclusions can be drawn for the nuclear industry. Investments must be made now to extend the operation life of nuclear reactors and/or develop an industrial program to build new reactors. Investment in a new nuclear station will necessarily involve state (or supranational[6]) intervention to open regulatory, budgetary and industrial doors[7] to nuclear energy. Until now these doors have been closed to the nuclear sector, unlike gas and renewable energy (p. 978). Secondly, it is necessary to consider the appropriate financing framework for a new nuclear power station; the implementation of which will depend on the context of each country [8].

Until very recently, nuclear energy was the subject of much resistance in public opinion. This multifactorial resistance had a lasting impact on its potential for deployment in energy systems. The main limiting factor in the decarbonization potential of nuclear energy is the divide it causes concerning radioactivity and nuclear accidents, as the IPCC addresses in its report (p.978). Nevertheless, there has been a sustained change in public opinion concerning nuclear energy, and the energy crisis coupled with the Russian invasion of Ukraine are reshaping nuclear power for many countries (such as Belgium). The debate has shifted from “nuclear risk” to issues of sovereignty, price control and reduced dependence on fossil fuels, including Russian gas. The IPCC suggests that this lengthy list of criteria skews very heavily in favor of nuclear energy (p.979). In this context, absent in the IPCC report due to the recent nature of events, it is clear that new positive prospects are emerging for nuclear energy.

Published on 14 March 2022

[1] Annual greenhouse gas emissions over the 2010-2019 period are higher on average than over the last decade, but the growth of these emissions is lower. Thus, there is a sentiment of having shown “better effort” in this last decade.

[2] The term “demand reduction” appears 56 times in the full report.

[3] GHG emissions per unit of “produced” energy, or more scientifically, energy which is extracted from the environment for our use.

[4] “Public and private finance flows for fossil fuels are still greater than those for climate adaptation and mitigation (high confidence)”.

[5] Between 2010 and 2019, solar costs fell by 85%, onshore wind costs by 55%, and lithium-ion battery costs by 85%.

[6] i.e. The EU taxonomy

[7] https://www.linkedin.com/posts/voix-du-nucleaire_giec-raezchauffementclimatique-efficacitaez-activity-6917049751569883136-Xx7E/?utm_source=linkedin_share&utm_medium=member_desktop_web

[8] https://www.sfen.org/avis/etude-sfen-comment-financer-le-renouvellement-du-parc-nucleaire/